Securing your family’s financial future requires careful planning. Estate planning, a crucial component of wealth management, goes beyond simply drafting a will. It involves strategically managing assets, minimizing tax liabilities, and ensuring a smooth transfer of wealth across generations. This comprehensive process considers various factors, including family dynamics, legal jurisdictions, and individual risk tolerance, to create a tailored plan that protects and preserves your legacy.

This exploration delves into the core principles of estate planning within a wealth management context, examining strategies for high-net-worth individuals and families. We will discuss the role of trusts, insurance products, and tax optimization techniques in building a robust estate plan. Furthermore, we will address the ethical responsibilities of wealth managers and the importance of transparent communication throughout the process.

Defining Estate Planning in Wealth Management

Estate planning, within the context of wealth management, is the comprehensive process of arranging for the administration and distribution of a person’s assets after their death. It’s not merely about avoiding taxes; it’s about ensuring the smooth transfer of wealth according to the individual’s wishes, protecting their family’s financial future, and minimizing potential legal disputes. This involves considering various legal, financial, and tax implications to achieve the desired outcome for the individual and their beneficiaries.

Core Principles of Estate Planning in Wealth Management

The core principles revolve around understanding the client’s goals, assets, and liabilities, and then crafting a strategy to achieve those goals. This includes identifying and mitigating potential risks, such as estate taxes, probate delays, and family conflicts. Effective estate planning involves a holistic approach, considering all aspects of the client’s financial life and future projections. A key aspect is ensuring that the client’s wishes are clearly articulated and legally sound.

Flexibility is also important, as life circumstances and tax laws can change.

Key Objectives of Estate Planning for High-Net-Worth Individuals

High-net-worth individuals (HNWIs) face unique challenges in estate planning. Their primary objectives often include minimizing estate taxes, preserving family wealth across generations, protecting assets from creditors, and ensuring a smooth transition of ownership to heirs. They also need to consider the complexities of managing large and diverse asset portfolios, including businesses, real estate, and investments. Charitable giving and legacy planning are also often significant objectives for this group.

Estate Planning Strategies for Different Family Structures

Estate planning strategies must adapt to different family structures. For example, a single individual with no children may focus on charitable giving or leaving their assets to a specific individual or organization. A couple with minor children will likely prioritize providing for their children’s care and education, potentially utilizing trusts to manage assets until the children reach adulthood.

Families with blended families or complex relationships may need to use more sophisticated strategies, such as irrevocable life insurance trusts, to protect assets and ensure fair distribution. The presence of a family business adds another layer of complexity, requiring careful consideration of succession planning.

Common Estate Planning Documents and Their Purposes

A variety of legal documents are crucial for effective estate planning. Understanding their purpose and implications is vital.

| Document Name | Purpose | Key Considerations | Potential Tax Implications |

|---|---|---|---|

| Will | Specifies how assets will be distributed after death. | Clarity of language, beneficiary designation, and consideration of all assets. | Estate taxes may apply depending on the value of the estate and applicable laws. |

| Trust | Manages assets for beneficiaries according to the grantor’s instructions. Various types exist (e.g., revocable, irrevocable). | Choice of trust type, trustee selection, and asset allocation within the trust. | Tax implications vary significantly depending on the trust type and its structure. Proper structuring can minimize tax burdens. |

| Power of Attorney | Authorizes another person to manage financial and legal affairs if the grantor becomes incapacitated. | Choosing a reliable and trustworthy agent, specifying the scope of authority. | Generally no direct tax implications, but indirect implications can arise depending on how the agent manages assets. |

| Healthcare Directive/Living Will | Specifies the grantor’s wishes regarding medical treatment if they become incapacitated. | Clarity of instructions, designation of healthcare proxy. | No direct tax implications. |

Wealth Management Strategies Integrated with Estate Planning

Effective estate planning is not merely about distributing assets after death; it’s a crucial component of comprehensive wealth management, ensuring the preservation and growth of your assets while aligning with your family’s long-term financial goals. Integrating wealth management strategies into your estate plan allows for a holistic approach, maximizing the benefits for both current and future generations. This involves strategically employing various tools and techniques to safeguard and transfer wealth efficiently and effectively.

The Role of Trusts in Preserving and Transferring Wealth

Trusts serve as powerful tools for preserving and transferring wealth across generations, offering significant tax advantages and asset protection. They act as separate legal entities, holding assets on behalf of beneficiaries. This separation shields assets from creditors, potential lawsuits, and even the mismanagement of beneficiaries. Furthermore, careful trust design can minimize estate and inheritance taxes, allowing a greater portion of the wealth to be passed down.

Different trust structures cater to diverse needs and objectives, providing flexibility in managing and distributing assets according to a predetermined plan.

Utilizing Insurance Products in Estate Planning

Insurance products play a vital role in a comprehensive estate plan, primarily addressing liquidity needs and protecting against unforeseen circumstances. Life insurance, for example, can provide the necessary funds to pay estate taxes, cover outstanding debts, or fund future educational expenses for heirs. Disability insurance offers protection against income loss due to illness or injury, ensuring financial stability for the family.

Properly integrated, insurance policies can mitigate financial risks and ensure the smooth transfer of wealth, even in the face of unexpected events.

Types of Trusts

The choice of trust depends heavily on individual circumstances and objectives. Understanding the differences is crucial for selecting the most appropriate structure.

- Revocable Trusts: These trusts allow the grantor (the person creating the trust) to retain control over the assets and make changes or even revoke the trust entirely during their lifetime. This offers flexibility but provides less asset protection than irrevocable trusts.

- Irrevocable Trusts: Once established, the grantor relinquishes control over the assets, offering significant asset protection from creditors and lawsuits. This structure often provides substantial tax advantages, but the lack of control is a significant consideration.

- Charitable Trusts: These trusts are designed to support charitable organizations, providing tax benefits for the grantor while benefiting a chosen charity. Different types of charitable trusts offer varying levels of control and tax advantages.

Hypothetical Estate Plan for a High-Net-Worth Family

Consider a family with significant assets in real estate, investments, and a successful business. Their estate plan could incorporate:

- Irrevocable Life Insurance Trust (ILIT): To hold life insurance policies, shielding the death benefit from estate taxes.

- Family Limited Partnership (FLP): To transfer ownership of the business to future generations while minimizing gift and estate taxes.

- Revocable Trust: To manage and protect assets during their lifetime, providing flexibility while facilitating a smoother transition of assets after death.

- Grantor Retained Annuity Trust (GRAT): To transfer assets to heirs while minimizing gift and estate taxes by leveraging the growth of assets within the trust.

This plan aims to minimize taxes, protect assets, and ensure a smooth transfer of wealth to the next generation, reflecting a coordinated strategy of wealth preservation and distribution.

Tax Implications of Estate Planning

Effective estate planning is inextricably linked to minimizing tax liabilities associated with wealth transfer. Understanding the tax implications in different jurisdictions is crucial for ensuring a smooth and efficient transition of assets to beneficiaries. Failure to consider these implications can lead to significant financial burdens on heirs and erode the value of the estate considerably.

Key Tax Considerations Across Jurisdictions

Estate and inheritance taxes vary significantly across jurisdictions. Some countries, like the United States, impose both estate taxes (on the value of the estate at death) and gift taxes (on gifts made during one’s lifetime). Others may only have inheritance taxes, levied on the beneficiaries receiving the inheritance. The tax rates and applicable exemptions also differ widely. For example, the US has a significant estate tax exemption, while some European countries have lower exemptions or no estate tax at all.

Canada, for instance, abolished its federal estate tax in 2016, leaving only provincial succession duties to be considered. Careful consideration of the specific tax laws of the relevant jurisdiction(s) is paramount. Professional advice from a tax specialist familiar with international tax law is often necessary when dealing with assets and beneficiaries in multiple countries.

Impact of Estate Taxes on Wealth Transfer

Estate taxes directly reduce the amount of wealth transferred to heirs. The tax is calculated on the net value of the estate after deducting allowable deductions and expenses. This means a substantial portion of the accumulated wealth may be lost to taxes, potentially leaving beneficiaries with less than anticipated. The impact is particularly pronounced in estates with high net worth, where the tax liability can reach millions of dollars.

For example, an estate valued at $10 million in the US, before considering the exemption, could face a significant tax burden depending on the applicable rate. Careful estate planning strategies can mitigate this impact, ensuring a larger portion of the wealth is passed on to the intended beneficiaries.

Gift Tax Implications and Minimization Strategies

Gift taxes are levied on gifts made during one’s lifetime, exceeding certain annual gift tax exclusions. These exclusions vary by jurisdiction, providing a threshold for gifts that are tax-free. Strategies for minimizing gift tax liabilities include utilizing the annual gift tax exclusion to make smaller, regular gifts, gifting assets that have appreciated less, and making gifts to multiple beneficiaries to spread out the tax impact.

Furthermore, establishing trusts can offer significant tax advantages, allowing for controlled distributions and potentially shielding assets from gift and estate taxes. Careful consideration of gifting strategies requires professional tax and legal advice, as improper planning can lead to unintended tax consequences.

Estate Planning Structures for Tax Minimization

Strategic estate planning can significantly reduce overall tax liabilities. Various strategies can be employed, depending on individual circumstances and goals.

| Tax Strategy | Description | Effect on Estate Tax | Effect on Gift Tax |

|---|---|---|---|

| Charitable Giving | Donating assets to qualified charities. | Reduces taxable estate value. | Potentially deductible from gift tax liability. |

| Irrevocable Life Insurance Trusts (ILITs) | Life insurance policies held within a trust structure. | Keeps death benefit out of the taxable estate. | No immediate gift tax, but gift tax may apply on funding the trust. |

| Grantor Retained Annuity Trusts (GRATs) | Trust structure where the grantor receives an annuity payment. | Reduces taxable estate value by transferring future appreciation. | Gift tax on the present value of the remainder interest. |

| Family Limited Partnerships (FLPs) | Business structure that limits liability and facilitates wealth transfer. | May reduce estate tax valuation through discounts. | Gift tax implications on initial contribution. |

Ethical Considerations in Wealth Management and Estate Planning

Ethical considerations are paramount in wealth management and estate planning, demanding a high level of professionalism and integrity from advisors. The fiduciary duty owed to clients necessitates prioritizing their best interests above all else, demanding careful consideration of potential conflicts and a commitment to transparency and open communication. Failure to adhere to these ethical standards can lead to legal repercussions, reputational damage, and the erosion of client trust.

Responsibilities of Wealth Managers in Estate Planning Advice

Wealth managers act as fiduciaries, meaning they have a legal and ethical obligation to act in the best interests of their clients. This responsibility extends to providing sound, unbiased advice on estate planning strategies, ensuring the client fully understands the implications of their choices. This includes a thorough assessment of the client’s financial situation, family dynamics, and long-term goals, followed by the presentation of options tailored to their specific needs.

Advisors must disclose any potential conflicts of interest and avoid recommending products or services solely for personal gain. They should also maintain client confidentiality and protect sensitive information. For example, a wealth manager must not recommend a specific investment product because they receive a higher commission, but rather choose the most suitable option for the client’s portfolio and estate plan.

Transparency and Client Communication in Estate Planning

Transparency and open communication are cornerstones of ethical estate planning. Clients must receive clear, concise explanations of complex financial concepts and legal jargon. This involves using accessible language, avoiding technical terms whenever possible, and providing ample opportunity for questions and clarification. Regular updates on the progress of the estate plan and any significant changes are crucial. For instance, if new tax laws are enacted that impact the client’s plan, the wealth manager has an ethical obligation to promptly inform the client and discuss the necessary adjustments.

This proactive approach ensures that clients remain informed and actively participate in the decision-making process.

Conflict Resolution Approaches in Estate Planning

Disputes among family members regarding inheritance are unfortunately common. Ethical wealth managers should proactively address potential conflicts by encouraging open communication and mediation. If disputes arise despite these efforts, different approaches to resolution can be considered. Negotiation, facilitated by the wealth manager, aims to reach a mutually acceptable agreement. Mediation involves a neutral third party to help facilitate communication and find common ground.

Arbitration involves a neutral third party making a binding decision. Litigation, as a last resort, involves legal action to resolve the dispute. The choice of approach depends on the nature and severity of the conflict and the willingness of the parties involved to cooperate. A wealth manager’s role is to guide the process fairly and ethically, always prioritizing the best interests of the client and their family, even in the face of disagreements.

Potential Ethical Dilemmas and Solutions

Several ethical dilemmas can arise in wealth management and estate planning. For example, a client may request a strategy that the advisor believes is not in their best interest, perhaps due to high risk or tax inefficiencies. The advisor must carefully explain the potential downsides, offering alternative solutions that align with the client’s goals while mitigating risks. Another dilemma might involve a conflict of interest, such as the advisor benefiting financially from recommending a particular product.

Full transparency and disclosure are crucial in such situations. If a conflict cannot be avoided, the advisor should seek independent advice or remove themselves from the situation entirely. Maintaining strict adherence to professional codes of conduct and seeking guidance from ethical review boards when necessary are essential steps in navigating these complexities. A further example is the challenge of managing a client’s estate when family members are involved in disputes.

The advisor must remain impartial and ensure all parties are treated fairly.

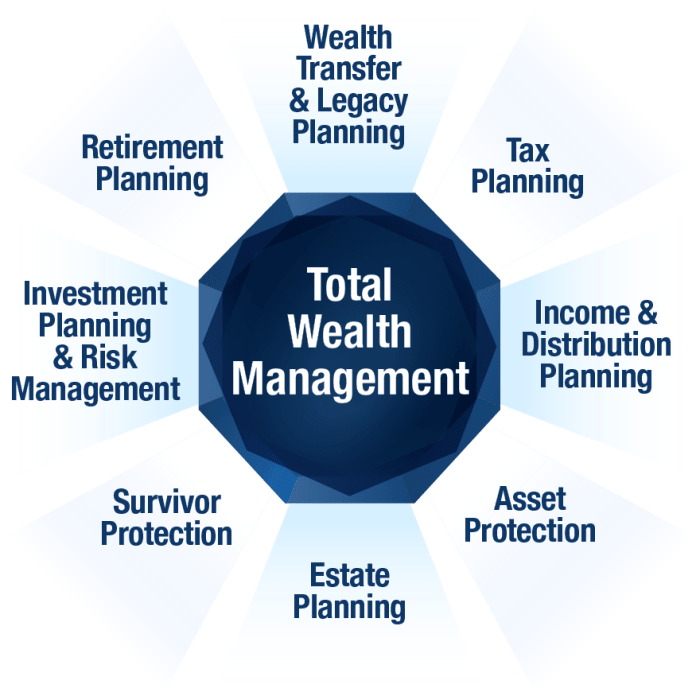

Wealth Management

Wealth management encompasses a significantly broader range of services than estate planning alone. While estate planning focuses on the distribution of assets after death, wealth management is a holistic approach to the ongoing stewardship and growth of an individual’s or family’s financial resources throughout their lifetime. It involves a comprehensive strategy that considers all aspects of financial well-being, from investment management and tax optimization to retirement planning and philanthropy.

Investment Strategies in Wealth Management

Wealth management utilizes a diverse array of investment strategies tailored to individual client needs and risk tolerance. These strategies aim to maximize returns while mitigating risk and achieving long-term financial goals. The selection of specific strategies depends on factors such as the client’s age, investment timeline, risk appetite, and financial objectives. Common strategies include active and passive investing, value investing, growth investing, and income investing.

Sophisticated strategies may also involve alternative investments like hedge funds, private equity, and real estate.

Risk Management and Portfolio Diversification

Effective risk management is paramount in wealth management. This involves identifying, assessing, and mitigating potential risks that could impact the client’s portfolio. A core principle is diversification, which aims to reduce risk by spreading investments across different asset classes, geographies, and sectors. This minimizes the impact of any single investment performing poorly. Sophisticated risk management techniques, such as hedging strategies and scenario planning, are often employed to protect against unforeseen events.

Example of a Diversified Investment Portfolio for a High-Net-Worth Individual

A diversified portfolio for a high-net-worth individual might consist of a mix of asset classes designed to balance growth potential with risk mitigation. For instance, a sample allocation could be:

| Asset Class | Allocation Percentage | Rationale |

|---|---|---|

| Equities (Domestic and International) | 40% | Provides long-term growth potential through exposure to a variety of companies across different markets. Diversification across geographies reduces reliance on any single economy’s performance. |

| Fixed Income (Government and Corporate Bonds) | 25% | Offers stability and income generation, acting as a counterbalance to the volatility of equities. Diversification across government and corporate bonds mitigates credit risk. |

| Real Estate (Direct Ownership and REITs) | 15% | Provides inflation hedge and potential for capital appreciation. A mix of direct ownership and Real Estate Investment Trusts (REITs) offers diversification within the real estate sector. |

| Alternative Investments (Private Equity, Hedge Funds) | 10% | Offers potential for higher returns and diversification beyond traditional asset classes, but also carries higher risk. Careful due diligence and selection are crucial. |

| Cash and Cash Equivalents | 10% | Provides liquidity for immediate needs and opportunities, and acts as a buffer during market downturns. |

This is a sample allocation and the actual percentages would be adjusted based on the individual’s specific circumstances, risk tolerance, and financial goals. A professional wealth manager would work closely with the client to create a customized portfolio that aligns with their unique needs.

Succession Planning in Family Businesses

Succession planning in family-owned businesses is a critical process that ensures the long-term viability and prosperity of the enterprise while managing the transition of ownership and control across generations. It’s a multifaceted undertaking, requiring careful consideration of both business and family dynamics. Failure to plan effectively can lead to significant challenges, including internal conflict, financial instability, and ultimately, the demise of the business.Effective succession planning mitigates these risks, fostering a smooth transition and preserving the legacy of the family business.

It involves a comprehensive strategy that addresses legal, financial, and emotional aspects of the transfer, ensuring the continued success of the business and the well-being of the family.

Challenges and Opportunities in Family Business Succession

Succession planning in family businesses presents unique challenges stemming from the intertwined nature of family and business relationships. These include emotional attachments to the business, differing visions among family members regarding the future direction of the company, and potential conflicts of interest between family members and non-family employees. However, successful succession planning also presents significant opportunities, including the preservation of family wealth, the continuation of a family legacy, and the creation of a sustainable and thriving business for future generations.

A well-executed plan can strengthen family relationships, improve business performance, and create a more secure future for all stakeholders.

Effective Succession Planning Strategies for Family Businesses

Several strategies can enhance the effectiveness of succession planning. Open communication and family meetings are crucial to fostering transparency and addressing concerns proactively. A formal succession plan, outlining roles, responsibilities, and timelines, provides clarity and reduces ambiguity. Mentorship programs can facilitate the development of future leaders within the family, providing them with the necessary skills and experience.

Professional advisors, including lawyers, accountants, and financial planners, provide invaluable expertise in navigating the legal, financial, and tax implications of the succession process. Finally, the establishment of a family council or governance structure can help manage family dynamics and ensure that decisions are made in the best interests of both the family and the business. For example, a family with a construction business might implement a mentorship program where the next generation learns the trade alongside experienced employees, gradually assuming more responsibility.

Approaches to Transferring Ownership and Control

Different approaches exist for transferring ownership and control in family businesses. A gradual transfer of ownership and management responsibilities allows for a smoother transition, minimizing disruption to the business. This approach often involves a phased retirement of the current owner, with the successor gradually assuming more control over time. Alternatively, a complete transfer of ownership can occur at a specific point in time, such as upon the retirement or death of the current owner.

This approach may be more suitable for businesses with clear successors and well-defined plans. Finally, a sale of the business to an external party can be considered, though this option often represents a departure from the family’s long-term vision and may lead to a loss of family control and legacy. The choice of approach depends on various factors, including the size and complexity of the business, the family’s goals, and the capabilities of the successor.

Hypothetical Succession Plan for a Family-Owned Bakery

Let’s consider a hypothetical succession plan for “Grandma’s Bakery,” a family-owned bakery established 50 years ago by Maria. Maria, now 70, wishes to retire within the next five years. Her daughter, Isabella, 40, has expressed interest in taking over the business.The plan would involve several key steps:

1. Assessment

A thorough assessment of the bakery’s financial health, operational efficiency, and market position would be conducted.

2. Mentorship

Isabella would undergo a mentorship program, learning all aspects of the business from Maria and experienced employees. This would include baking techniques, customer relations, and financial management.

3. Training

Isabella would receive formal training in business management and leadership.

4. Financial Planning

A detailed financial plan would be developed, outlining the transfer of ownership and the management of family wealth. This might include a gradual transfer of shares or a sale of the business to Isabella at a predetermined price.

5. Legal Documentation

All legal documents, including wills, trusts, and partnership agreements, would be updated to reflect the succession plan.

6. Family Council

A family council would be established to facilitate communication and resolve any potential conflicts among family members.

7. Contingency Planning

A contingency plan would be developed to address unforeseen circumstances, such as Isabella’s inability to assume leadership or the unexpected death of Maria.This plan ensures a smooth transition, preserving the bakery’s legacy and safeguarding the family’s financial future. The gradual transfer of responsibilities minimizes disruption, allowing Isabella to develop her skills and build confidence. The establishment of a family council promotes open communication and addresses potential conflicts proactively.

Effective estate planning is not a one-size-fits-all solution. It requires a proactive and collaborative approach, involving careful consideration of individual circumstances and a commitment to long-term financial security. By integrating sound estate planning strategies with a broader wealth management plan, individuals and families can safeguard their assets, minimize tax burdens, and ensure a legacy that aligns with their values and aspirations.

The process, while complex, offers the peace of mind that comes with knowing your family’s future is well-protected.

FAQ Corner

What is the difference between a revocable and irrevocable trust?

A revocable trust can be modified or terminated by the grantor, while an irrevocable trust cannot be changed after its creation. Irrevocable trusts offer greater asset protection and tax advantages but lack the grantor’s control.

How often should I review my estate plan?

It’s recommended to review your estate plan at least every three to five years, or more frequently if there are significant life changes (marriage, divorce, birth, death, etc.).

What is probate, and how can I avoid it?

Probate is the legal process of validating a will and distributing assets. Using trusts and other estate planning tools can significantly reduce or eliminate the need for probate.

Do I need an estate plan if I don’t have a lot of assets?

Even if you have modest assets, an estate plan is crucial for ensuring your wishes are followed regarding the distribution of your property and the care of your dependents.